JUBILANT PHARMOVA – Q4 & FULL YEAR FY26 RESULTS

On track towards Vision 2030

Solid Revenue growth across all business segments

Onboarded one of the World’s largest Oncology products on CDMO Sterile Injectables Spokane, Line 3

1. Normalised PAT is after adjusting for exceptional items and corresponding tax.

The Board of Jubilant Pharmova Limited met today to approve financial results for the quarter and full year ended Mar 31, 2026. The board has proposed a dividend of Rs. 5 per equity share.

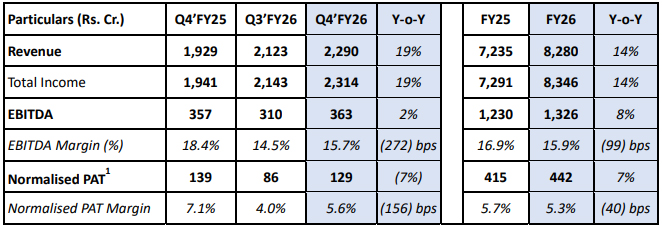

Commenting on the Company’s performance for FY26, Mr. Shyam S Bhartia, Chairman Jubilant Pharmova Limited and Mr. Hari S Bhartia, Co-Chairman & Non-Executive Director, Jubilant Pharmova Limited said, “We are pleased to announce revenue of Rs. 8,280 Cr. for FY26, which reflects a solid growth of 14% on YoY basis. Revenue growth is particularly driven by incremental revenue generation from the new & third line in CDMO Sterile Injectable business. We expect this growth momentum to strengthen as we move in the next financial year. EBITDA for the year grew by 8% to Rs.1,326 Cr. due to improved performance across all segments except Radiopharmaceuticals, which was affected due to lower production of SPECT products at CMO Montreal. Normalised PAT for the year grew by 7% to Rs. 442 Cr. due to improved operating performance of the business. As we are consciously investing in businesses to secure future growth, Net Debt / EBITDA remains range bound at 1.3x in Mar’26, as compared to 1.1x in Mar’25.

During FY26, we saw exceptional growth momentum in the Ruby-Fill® installs. In the Allergy Immunotherapy business, we witnessed increase in demand from both markets, US and Outside US. In the CDMO Sterile Injectables business, we saw one of the fastest revenue ramp up across the industry, at Line 3 in Spokane. We are proud to share that we have onboarded one of the World’s largest Oncology products on our Line 3. In the CRDMO business, we announced a strategic partnership with Pierre Fabre, France, to expand our footprint in Europe in areas such as biologics (mAbs) and Antibody-Drug Conjugates (ADCs). We also combined drug discovery business and API Business in a single entity to improve operational efficiency & increase the brand recall of the business. In the Generics Business, we delivered a year of strong growth and double digit operating profitability. Lastly, in our Proprietary Novel drugs business, we continue to make progress in JBI-802 and JBI-778 clinical trials.

During the year, particularly in the second half, we witnessed a decline in EBITDA margins, primarily due to the temporary shutdown of our CDMO Sterile Injectables facility in Montreal, for remediation, following FDA observations. We anticipate EBITDA margins to strengthen from H2’FY27 onwards post stabilisation of production at Montreal, effectively offsetting higher depreciation costs and driving net profit growth.”

Q4’FY26 Financial Highlights

- Revenue grew by 19% on a YoY basis to Rs. 2,290 Cr. on the back of growth in Radiopharma, Allergy Immunotherapy, CDMO Sterile Injectables and Generics.

- EBITDA increased by 2% on a YoY basis to Rs. 363 Cr. EBITDA margins decreased YoY due to the shortage in supply of SPECT products in Radiopharma and under absorption of costs in CMO Montreal.

- Normalised PAT stood at Rs. 129 Cr. Normalised PAT decreased marginally YoY due to increase in depreciation and interest cost.

Segmental Business Performance

Radiopharma - Leading Radiopharmaceutical manufacturer & 2nd largest Radiopharmacy network in the US

Radiopharmaceuticals FY26 revenue grew by 10% to Rs. 1,178 Cr. and EBITDA for the year stood at Rs. 480 Cr. Q4’FY26 and FY26 EBITDA margins decreased YoY due to one-time negative impact of lower production of certain SPECT products at CMO Montreal. We have successfully conducted media fills at CMO Montreal, and the commercial batch production will start in the current quarter. As supply resumes, Revenue and EBITDA will normalize from H2’FY27 onwards. The business continues to maintain a strong position in the high margin SPECT imaging product portfolio. In the Ruby-Fill®, as we can demonstrate superior value proposition against competition, we are able to attract new channel partners. Our Ruby-Fill® install base has grown by 35% in FY26 vs 21% in FY25. This improved scale is also helping to increase EBITDA margins in this product category. We are on track to introduce multiple new products in the PET and SPECT imaging from FY28 to FY29. The dosing for Phase 2 clinical trial for MIBG is complete and we expect to do NDA filing by H2’FY27.

Radiopharmacy FY26 revenue grew by 9% YoY to Rs. 2,512 Cr. EBITDA for the year grew by 20% to Rs. 36 Cr. Last year, two of our PET manufacturing facilities had started distributing PYLARIFY®, which is an industry leading prostate cancer diagnostic imaging agent. We continue to see increase in revenue from our three PET manufacturing facilities. We have also started distributing Pluvicto, which is a leading radiopharmaceutical to treat prostate cancer.

The proposed investment of US$ 50 million in PET manufacturing network is underway. This investment will take the overall PET radiopharmacy network to Nine (9) sites, thereby strongly positioning Jubilant Pharmova’s radiopharmacy network as the second largest in the US and shall drive the future business growth.

Allergy Immunotherapy - No. 2 in the US Sub-Cutaneous allergy immunotherapy market

As the sole supplier of Venom in the US, we are expanding the overall market by increasing customer awareness. In the US Allergenic extracts, we are working to increase revenues. We are also working to increase the penetration in the markets outside the US.

In FY26, revenues grew by 12% to Rs. 785 Cr., driven by strong growth in the US & outside US markets. EBITDA grew by 13% to Rs. 278 Cr. Full year EBITDA margin at 35% is in the normalised range.

CDMO Sterile Injectables – Leading contract manufacturer in North America, serving top global innovators

FY26 revenue grew by 38% to Rs. 1,755 Cr. due to incremental revenue from Line 3. EBITDA grew by 8% on YoY basis to Rs. 314 Cr. EBITDA margins were lower YoY due to shutdown of Montreal facility in Q2 & Q3, and due to under absorption of costs due to lower production.

At the Spokane facility, the capacity expansion program remains on track. Following the launch of our third Sterile Fill & Finish line (Line 3) in Q2’FY26, we are successfully ramping up revenues from technology transfer programs. Currently, 10+ products across multiple formats and vial sizes are undergoing technology transfer on Line 3. We are happy to share that we have onboarded one of the world’s largest oncology products on Line 3. Commercial batch production is expected to commence in late FY27, subject to FDA approval of these products. Revenue at Spokane for FY26 grew by 48% to Rs. 1,714 Cr. and EBITDA grew by 59% to Rs. 463 Cr. EBITDA margins also expanded by 190 basis points to 27%.

Considering the new tariffs imposed by the US Government, large innovator pharmaceutical companies are increasingly seeking high-quality, US-based manufacturing, specifically, those with significant capacities with isolator technology. As a result, we are seeing strong traction in Requests for Proposals (RFPs) for the new lines. The next phase of capacity expansion—Line 4—is also progressing as planned. We expect Line 4 to start generating technology transfer revenues by Q4’FY27

At Montreal facility, as we move into FY27, initial focus is to stabilize production for Radiopharmaceutical products and then we shall continue to produce for other customers and also target to reduce EBITDA losses. In the medium term, we anticipate that the new isolator-based fill-and-finish line (Line 5) will start generating revenues from FY29 onwards, thereby supporting the site for a profitable future growth.

CRDMO – Indian leader for integrated drug discovery & a formidable API player

In FY26, the Drug Discovery business revenue grew by 15% to Rs. 654 Cr. Revenue continues to increase due to increase in revenue from large pharma customers. EBITDA for the year grew by 11% to Rs. 151 Cr. In the short term, we expect competitive intensity to increase in the large-pharma customer segment, while demand conditions in the biotech segment are expected to improve. In the medium term, we expect to deliver healthy revenue growth & steady margins.

In the API business, revenue for FY26 stood at Rs. 564 Cr. EBITDA for the year stood at Rs. 83 Cr. Revenue and EBITDA margins decreased YoY due to the industry wide pricing pressure. We are consciously moving the revenue mix towards profitable products. Going forward, we expect the custom manufacturing revenue mix to drive the utilisation.

We have completed the sale and transfer of API Business to Jubilant Biosys Limited, a wholly owned subsidiary of the company. This transaction has resulted in housing of the drug discovery business and CDMO API business in a single business entity. This combined platform will improve the operational efficiency in the business and lead to superior brand recall of “Jubilant Biosys Limited” as the provider of end-to-end CRDMO services by the large pharmaceutical & biotech customers. The transaction will also help to improve asset utilisation of API business by improving the revenue mix towards custom manufacturing & CDMO.

Generics – Building a growing, profitable & agile business model

In FY26, the Generics business revenue grew by 13% to Rs. 774 Cr. EBITDA for the year grew by 250% to Rs. 83 Cr. EBITDA margins increased by 7.2 percentage points. Looking ahead, we expect sustained progress toward the Generics Vision 2030 shared previously.

Proprietary Novel Drugs – Innovative biopharmaceutical company developing breakthrough therapies

The global clinical trials for our lead programs, Phase I/II trial for JBI -802 for Essential Thrombocythemia (ET) and other Myeloproliferative Neoplasms (MPN) and Phase I trial for JBI -778 for non-small cell lung cancer (NSCLC) and highgrade Glioma are actively enrolling patients and progressing in line with our expectations.

About Jubilant Pharmova Limited

Jubilant Pharmova Limited is an integrated global pharmaceutical company engaged in Radiopharma, Allergy Immunotherapy, Contract Development and Manufacturing of sterile injectable, Contract Research Development and Manufacturing, Generics and Proprietary Novel Drugs businesses. With a network of 45 radiopharmacies in the USA, the Radiopharma business is engaged in manufacturing and supply of radiopharmaceutical products and services. The Allergy Immunotherapy business is involved in the manufacturing and supply of allergic extracts and venom products in the USA and other markets such as Canada, Europe and Australia. Contract Development and Manufacturing of sterile injectables, with facilities in Spokane, USA, and Montreal, Canada, delivers end-to-end manufacturing solutions, including sterile fill-and-finish injectables (liquid and lyophilized), comprehensive ophthalmic products (liquids, ointments and creams) and ampoules. Contract Research Development and Manufacturing business provides end-toend drug discovery and development services to the pharmaceutical and biotech industries through three world class research centres (two in India and one in France) and a US FDA approved, Active Pharmaceutical Ingredients manufacturing facility in Nanjangud, Karnataka. The Generics business focuses on development, manufacturing and distribution of Solid Dosage Formulations through multiple manufacturing facilities that cater to all the regulated market including USA, Europe and other geographies. Proprietary Novel Drugs is an innovative biopharmaceutical business developing breakthrough therapies in the area of oncology and auto-immune disorders. Jubilant Pharmova has a team of around 5,500 multicultural people across the globe. The Company is well recognised as a ‘Partner of Choice’ by leading pharmaceuticals companies globally. For more information, please visit:

www.jubilantpharmova.com.

For more information, please contact:

Disclaimer

Statements in this document relating to future status, events, or circumstances, including but not limited to statements about plans and objectives, the progress and results of research and development, potential product characteristics and uses, product sales potential and target dates for product launch are forward-looking statements based on estimates and the anticipated effects of future events on current and developing circumstances. Such statements are subject to numerous risks and uncertainties and are not necessarily predictive of future results. Actual results may differ materially from those anticipated in the forward-looking statements. Jubilant Pharmova may, from time to time, make additional written and oral forward looking statements, including statements contained in the company’s filings with the regulatory bodies and its reports to shareholders. The company assumes no obligation to update forward-looking statements to reflect actual results, changed assumptions or other factors.